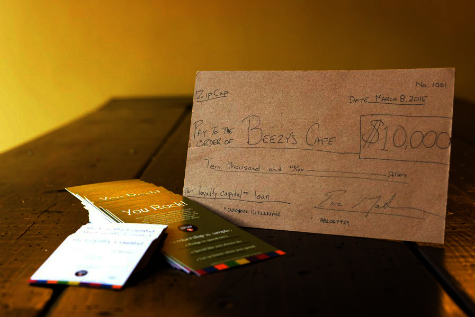

In spite of the billboards around town by local banks claiming to support homegrown businesses, the truth is, when our small “mom and pop” stores need capital, it’s almost impossible to come by. When a local restaurant, for instance, needs capital to grow, or to make it through lean times, there are few options, in spite of all the rhetoric to the contrary. Thankfully, there are a number of small business proponents out there in the world who are looking to remedy this, trying to find ways to get working capital into these small, local entities so that they can thrive and grow… and break free from the predatory lenders who have made it their business to prey on small business owners. And one of these folks, Evan Malter, the founder of ZipCap, has been spending quite a bit of time in Michigan lately, working with our friend Bee Roll, the owner of Ypsilanit’s much beloved Beezy’s Cafe, to secure more favorable lending terms. Here’s Evan on how they accomplished it by demonstrating to lenders that Beezy’s had a loyal customer base, and how, going forward, the idea of Loyalty Capital™ could help save America’s independent businesses. [below: Evan presents Bee with a hand-drawn check at the completion of the Beezy’s membership drive]

[note: This is the continuation of a conversation that began a few weeks ago on AM 1700’s Saturday Six Pack, where Evan and Bee discussed how they’d come to find one another, among other things.]

MARK: Here, to start with, is what I think I know about ZipCap… And feel free to jump in and correct me if any of this isn’t correct, Evan… ZipCap exists in order to put working capital into the hands of small retail businesses that would struggle to stay afloat, let alone grow, without it. ZipCap does this by demonstrating to investors that risk is decreased if said business has a loyal client base dedicated to spending a certain amount with them annually. I that pretty close?

MARK: Here, to start with, is what I think I know about ZipCap… And feel free to jump in and correct me if any of this isn’t correct, Evan… ZipCap exists in order to put working capital into the hands of small retail businesses that would struggle to stay afloat, let alone grow, without it. ZipCap does this by demonstrating to investors that risk is decreased if said business has a loyal client base dedicated to spending a certain amount with them annually. I that pretty close?

EVAN: It’s a good start. In the simplest terms – we are connecting local businesses to affordable capital. However, it’s important to note the bigger picture. We empower more than just the businesses. We intend to empower entire communities to rally for the businesses they want to have in their neighborhoods. In that same spirit, we feel strongly that, by engaging the community in the ZipCap process, we are strengthening the business with more than just financial capital.

To avoid confusion, I’d love to explain the model a little more specifically. Through ZipCap, customers who already intend to spend at a certain business can pledge that support without any pre-payment or investment… they are simply saying, “I will come back.” ZipCap then turns those pledges into something we call Loyalty Capital™, which serves as a sort of line of credit for the business. And this money is available once a business is able to rally 100 loyal customers.

MARK: Is it safe to say that a lot, if not most, small, independent businesses in America fail because they lack access to the funds necessary to keep them afloat during lean times, or cover unexpected expenses?

EVAN: It is definitely safe to say that most independent businesses lack access to such funds. Since 2008, banks have basically abandoned these smaller businesses. Access to just $10,000 to $20,000 can be the difference between failing and thriving.

MARK: You’ve been spending quite a bit of time recently in Ypsilanti, as Beezy’s is one of your first real-world tests of the ZipCap concept. And, as I understand it, of all of the tests that you currently have running, Beezy’s was the first to reach the goal of having 100 of their regular customers pledge support (promising to spend at least $475 over the next year at the restaurant).

EVAN: Yep. I‘ve been here quite a bit, and, I won’t lie, I’m happy the weather is warming up. I’ve loved getting to know the community and this place called Ypsi. On your radio show the other night, I said “When I met Bee, I knew I wanted her to be my first.” That obviously didn’t come out just right, but I guess that’s the nature of live radio. Possible misinterpretations aside, I did mean what I said, and now, in retrospect, I’d add that I am glad that Ypsi was the community where it happened. When I started the journey to create ZipCap, it was entrepreneurs like Bee and communities like yours that I had in mind. We want to empower the people who are passionate about what they’re doing and the communities that are embracing their unique character and identity. Bee and Ypsilanti will forever have a special place in my heart.

Bee and her members were indeed the first to reach the 100-member goal, but, to be fair to the other pilots, not all were running the program in the same way as Bee… and frankly… Bee is a superstar.

MARK: So, once Beezy’s reached 100 members you were then able to go to lenders to negotiate the line of credit?

EVAN: Actually, that’s not quite how it works. The terms of the loan are known and guaranteed in advance of the member drive. Once a business owner rallies 100 members, the money is immediately made available to them. ZipCap is not shopping these loans around after the fact. We find the lenders in advance. Those lenders have trust in this new form of underwriting and are prepared to deploy capital when that criteria is met. [below: The hastily scrawled check presented to Bee]

MARK: By way of context, it’s probably worth noting that, prior to entering this deal with ZipCap, Bee’s only option, having been turned away by local banks, was to borrow money from a predatory lender when she needed money to get Beezy’s through unforeseen events… predatory lenders who were lending her money at an annual rate in excess of 80%. By comparison, what interest rates can businesses working through ZipCap expect?

EVAN: Our rates currently range from 0.99% to 18.99%, and Beezy’s is borrowing at a rate in the low single digits. Bee will pay less in interest over the course of a year than she was paying every couple weeks with her last loan.

MARK: What influences the rate on your end?

EVAN: ZipCap is all about putting the business owner back in control. If they can please their customers then they should have access to capital. We go a step further by rewarding their efforts with better rates and more access. The more Loyalty Capital™ that they can rally, the lower their rate and the higher their line of credit.

MARK: When you dropped by the radio show with Bee, you mentioned that you’d had some broadcasting experience, but I had no idea just how extensive that experience was until I looked you up on LinkedIn today and discovered that you were “the radio voice of the Hickory Crawdads, the Winston-Salem Warthogs, and the Greensboro Bats.” If I’d known, I would have asked you for some of your catch phrases… You did have catchphrases, right?

EVAN: You’re really putting me on the spot with this one. It’s been many years… I had some favorite things that I’d say, but was never really one for scripted lines. Some home runs require a “that one is long gone” and some are a simple “touch ‘em all” – it depends on the moment. The only thing that I repeated on each broadcast was the opening and closing line. I started with “Another Day, Another Ball Game” and closed with “There will always be another ballgame.” It’s kind of a “baseball is life” metaphor, but I may have been trying too hard with that.

MARK: Do you miss working in baseball?

EVAN: I definitely do. Who wouldn’t want to work at the ballpark every day? I am a person with no regrets, and I believe that our lives take the course they do for a reason. I had my fun in baseball, and now I’m pursuing another passion, and hopefully making a positive impact on the world. With that said, in the unlikely event that a Major League Club called and offered me a play-by-play job – I would have a decision to make.

MARK: When did the idea for ZipCap first come to you?

EVAN: The short answer is that the idea of ZipCap, and the passion and experience to make it happen, was decades in the making, but officially ZipCap was born a little over 2 years ago. We filed the patent for the business method (using customer loyalty as due diligence and “collateral” for a loan) in February of 2013 and incorporated the company soon after that.

MARK: OK, so what’s the long answer? What was the path that got you to that point two years ago when you started ZipCap?

EVAN: I’ve been a devout localist my entire life and believe passionately in local small businesses for all the obvious reasons. You’ve probably heard the stats about small businesses creating more than half of the jobs and being the primary driver for our economy. As an economist, I can’t ignore those things. To be honest, though, for me it’s about preserving the unique character of our communities and making it possible for people to pursue their passions, and, in doing so, sharing their passions with the rest of us. It’s about personal face-to-face relationships. It’s about being in Ypsi and knowing you’re in Ypsi and not Ann Arbor, or Detroit, or San Diego.

MARK: I wasn’t aware that you had an economics degree.

EVAN: Yeah, as you can see on my LinkedIn profile, my career has taken a few turns, but I truly believe that each one was leading towards ZipCap. I got an economics degree, but chose to avoid the traditional “Wall Street” route. (That was how I ended up in sports radio.) I did eventually work in finance, and I also founded a company that worked with Mom and Pops. Those experience all have an obvious link to ZipCap, but the six years that I spent living in Australia with my family made a huge impact as well. I was able to see America from the outside and live in a place where you get meat from the butcher, fruit from the fruit guy and flowers from the florist. In 2012, we were settling back into our life in America and my wife came home with groceries from a big box store. That was the day that ZipCap started taking shape. I was horrified to think about a world without the relationships, passion and character of local businesses. I knew there needed to be more ways to support passionate entrepreneurs and give the world more ways to rally for them.

As I dug into the issue, it became obvious very quickly that others felt the same way and it was exciting to explore all of the creative ways people were approaching the issue. It became clear that shifting money from Wall Street to Main Street would be central in any proper solution. I set out to learn as much as I could and played with ways for community members to invest in their favorite businesses. That was short lived, however, as I grew uncomfortable with the idea of shareholders for local businesses. I didn’t feel it was good for anyone in the ecosystem.

I realized that there was no shortage of capital in the world if we could prove decreased risk to an investor. The consumer in the community did not need to be that investor… they just needed to do what they were already good at doing… consuming. If we could foster and monetize their “intent to spend,” we could reward everyone in the ecosystem. With that revelation, ZipCap was truly born.

MARK: I’d like to follow up on something that you just said. “ I grew uncomfortable with the idea of shareholders for local businesses.” I’m curious as to why. I’ve always thought that local stock exchanges had promise.

EVAN: I want to be careful with this answer, because like you, I would love for people to invest locally and that is absolutely one of the end goals of ZipCap. I know, for instance, that we could create a sort of micro-bond that is debt-based and allows locals to comfortably invest in their community without requiring as much risk or research.

This answer could be another long one, but bear with me. At Columbia, I wrote a paper in which I suggested that Jack Welch had ruined America. It may sound extreme, but the idea was that shareholder value had become too important and that customer value was an after-thought. It’s why I love local businesses. For them, the customer and the community are the top priority. What would happen if the owner of the local pizza shop had to start thinking about shareholders and meeting quarterly numbers and dividends? Maybe he would source cheaper cheese and toppings. Maybe he would just use less cheese on those cheesy pizzas you love. Maybe he would fire a member of the wait staff, and make do with just two, even though he really needed three to properly serve his customers.

Even if they were able to avoid that fate, most small business owners still don’t want shareholders. They have started these businesses because they have a passion for the business and they have specific ideas concerning how things should be run. They want to make enough money to support the business, pay employees, and take a little home to support a family. These are lifestyle businesses. These are not businesses that should need to support the demand of shareholders.

The reverse side is also important to consider. Grandma should not be investing in a pizza shop because she likes the pizza. Throughout my career I have done a great deal of business valuation, and I can tell you that the proper due diligence required to make an investment in a local business is too much for most “local investors.” And, the truth is, If they did the research and saw the numbers – they’d likely flee back to Wall Street any way.

I think the possibilities and future of crowdfunding and local investing are enormous. I’m fearful, however, that if, as an industry, we’re irresponsible, we’ll do more harm than good, and lose this incredible opportunity to change the way that people invest.

Some amazing people around the country have worked to strengthen the shop local movement over the last decade. Local economies are getting stronger and more sustainable. We hope that we can further that movement and use it to create a responsible way to shift money from Wall Street to Main Street.

MARK: And how did you go about finding your investors, the people who are actually making these loans through ZipCap?

EVAN: I’m glad that you asked that question, because it is likely unclear and also speaks to the bigger picture. At launch, as we prove this concept, we have a core group of investors who like what we are doing and believe in this underwriting criteria to make small business loans. This works well in the short term, but we’re excited to have begun talks with other stakeholders like foundations, philanthropists and actual municipalities, looking for new ways to inject capital into their communities in a responsible and affordable way. If we can achieve our goal of creating a micro-bond, we would then feel comfortable opening up investment to any and all stakeholders, including individual members of the community. We hope that someday people could take $500 from their savings account and move it into an Ypsilanti fund that would lend to small businesses in town and earn a small interest rate of return.

EVAN: I’m glad that you asked that question, because it is likely unclear and also speaks to the bigger picture. At launch, as we prove this concept, we have a core group of investors who like what we are doing and believe in this underwriting criteria to make small business loans. This works well in the short term, but we’re excited to have begun talks with other stakeholders like foundations, philanthropists and actual municipalities, looking for new ways to inject capital into their communities in a responsible and affordable way. If we can achieve our goal of creating a micro-bond, we would then feel comfortable opening up investment to any and all stakeholders, including individual members of the community. We hope that someday people could take $500 from their savings account and move it into an Ypsilanti fund that would lend to small businesses in town and earn a small interest rate of return.

MARK: So, here’s a hypothetical. Let’s say there’s a university with a vested interest in their local community, like Eastern Michigan University, or the University of Michigan. It’s possible that they could, in the future, invest some of their endowment dollars into a fund that would make loans to businesses in their communities…

EVAN: Absolutely. We believe we are creating a new asset class of sorts. They could have some funds in large cap, some in small cap and some in ZipCap. If we do this right, investing in local businesses could be part of any investment portfolio. The fact that it will make their community, and the world a better place, would be a bonus.

MARK: So, how is ZipCap capitalized? And do you have enough money to grow, now that the concept has been somewhat proven? I mean, it will probably take a significant team of people, and some real capital, to do things like establish micro-bonds at the community level.

EVAN: Indeed. Part of our mantra at ZipCap is that “Access to capital is opportunity for impact.” We considered starting ZipCap as a non-profit, but decided that, if we could create a model that made money and attracted real investment, we could create something that could scale and truly change the world. At this point, we’re considered seed-stage and, along with some of my own money, we have an on-going raise from angel investors. We have a core team of amazing people in San Diego and Michigan who have been working on things, and that team is growing. We have some milestones that we hope to hit by the end of this year, at which point we intend to go out for a more significant raise. We are confident that we are on course to achieve our goals and grow the company and our impact.

MARK: So, what’s next for you? Where will you be focusing your energy now that the Beezy’s beta test has proven successful? Where, to use your metaphor, is tomorrow’s ballgame?

EVAN: We are really excited to make Michigan our proving ground for ZipCap. We’ve already begun conversations with organizations throughout the state interested in facilitating our relationship with local businesses. In the few days since I presented Bee with her check, I have gotten calls and emails from business owners in Ann Arbor and Ypsi who had heard what was happening at Beezy’s and wanted to learn more. I’ve spoken to a few and some things are in the works, but more will be revealed in the coming weeks. Think Local First has invited me to present to member businesses in April, and that will likely lead to a few more things here in the County. We’re still limiting the businesses that we take on, but soon we hope to be in a position to open the platform up to any business that is interested. It’s very exciting to be at this point, on the cusp of the next big steps for ZipCap.

[note: Photos of Evan and Bee in the AM 1700 studio are courtesy of Kate de Fuccio. All other photos, except for the cell phone shot at the top, which I took, were taken by Chris Stranad.]

3 Comments

UM and EMU would never invest in this. I like the idea, but they’re all about the financial return and they would never accept a 5% rate of return.

With the stock market going the way it has been, it will be difficult to pull money away for the purposes of buttressing our main street businesses. As that’s the case, I like that Evan is moving toward a model where entities with a vested interest would be underwriting loans, like local economic development organizations. I would be happy to see some LDFA funds diverted from SPARK for this purpose.

Zipcap and Beezy’s are getting some national love on the Locavesting site.

http://www.locavesting.com/featured/a-startup-aims-to-turn-customer-loyalty-into-cash-starting-with-a-beloved-michigan-cafe/

One Trackback

[…] article, you’d still like to know more about Loyalty Capital™ and how it works, check out the interview I did not too long ago with zipCap CEO Malter… For the time being, though, I’d just like for you to focus on this clip from the […]