It’s been a hell of a long time coming, but, on Tuesday of next week, uninsured Americans will finally have an opportunity to shop for health insurance coverage online, in government-administered marketplaces, as part of the Affordable Care Act. It took three and a half years, during which time the Republicans attempted to defund it 41 times, taking it all the way to the Supreme Court, but the health care legislation commonly referred to as Obamacare, is about to come into its own. (Components have been rolled out over the past few years, but it’s all been a prelude to what’s coming on October 1.) And, as you might expect, folks on the far right are going apoplectic. With their last, desperate attempt to defund the legislation having failed with yesterday’s ineffective filibuster initiated by Ted Cruz, it now seems as though they have no choice but to ramp up their disinformation campaign about how Obamacare will surely spell the end of freedom in America. (After quoting a tweet by Ashton Kutcher on the floor of the Senate, Cruz compared the passage of the Affordable Care Act to Neville Chamberlain’s appeasement of Hitler.)

Obama, perhaps a bit emboldened by Cruz’s failure to attract more than 18 Senators to his cause, has taken to the streets, attempting to drum up interest in these soon-to-be-rolled-out health care insurance exchanges. (For it to be successful, they need a lot of people, especially young people, signing up, and they’re ramping up the marketing accordingly.) “The closer we get, the more desperate they get,” Obama recently told a group in Maryland… And, here, with more on that speech, is a clip from the Associated Press.

…Obama didn’t call out any of his Republican opponents by name, but he laughingly taunted some of their arguments. He mentioned House Speaker John Boehner’s prediction right before the bill was signed into law in March 2010 that “Armageddon” was impending. He quoted Louisiana Rep. John Fleming, who said earlier this month that “Obamacare is the most dangerous piece of legislation ever passed in Congress.” He cited Minnesota Rep. Michele Bachmann’s appeal to colleagues on the House floor six months ago to “repeal this failure before it literally kills women, kills children, kills senior citizens.”

And he quoted New Hampshire state Rep. Bill O’Brien’s declaration in August that Obamacare is “a law as destructive to personal and individual liberty as the Fugitive Slave Act of 1850.” That was met by a chorus of gasps and boos from the largely black audience.

“Think about that. Affordable Health Care is worse than a law that lets slave owners get their runaway slaves back,” Obama said. “I mean, these are quotes. I’m not making this stuff up.”

“All this would be funny if it wasn’t so crazy,” Obama said…

And, speaking of crazy, our own Kerry Bentivolio took enough time away from his investigation into the mind-controling properties of jet exhaust to send out an unsourced warning to his constituents, which you can see to the right. I ran it by our friend Michigan Representative Jeff Irwin, and he responded with the following: “Unfortunately, Congressman Bentivolio isn’t a trusted source, and his assertion is the opposite of every piece of data I’ve seen.” Furthermore, Irwin encouraged people who wanted the real facts to use the calculator on the Keiser Foundation’s site, where you can plug in a variety of variables and see how much health care will cost under the new system.

And, speaking of crazy, our own Kerry Bentivolio took enough time away from his investigation into the mind-controling properties of jet exhaust to send out an unsourced warning to his constituents, which you can see to the right. I ran it by our friend Michigan Representative Jeff Irwin, and he responded with the following: “Unfortunately, Congressman Bentivolio isn’t a trusted source, and his assertion is the opposite of every piece of data I’ve seen.” Furthermore, Irwin encouraged people who wanted the real facts to use the calculator on the Keiser Foundation’s site, where you can plug in a variety of variables and see how much health care will cost under the new system.

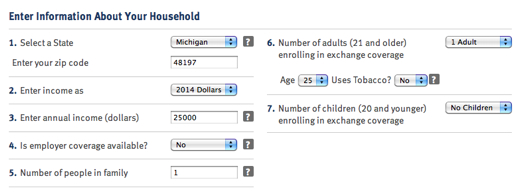

I just visited the Keiser site, as I was curious as to how a young person might fare. (Remember, Bentivolio said that a young male would be paying 52% more than he does today.) Here’s what I found.

My sample person is a 25 year old male in Ypsi, who makes $25,000, has no dependents, and doesn’t smoke.

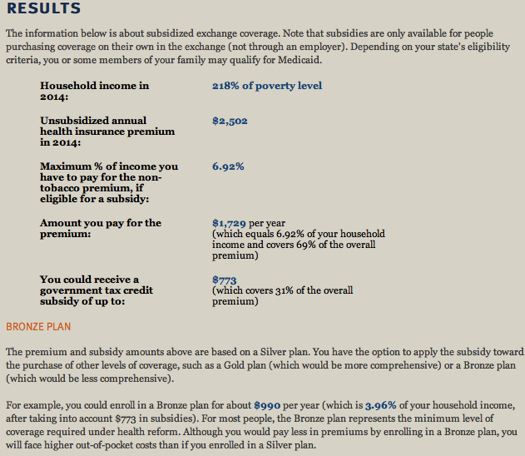

And, here, according to the Kaiser calculator, is what this 25 year old male would likely pay. (On Tuesday, when the Michigan exchange goes live, you’ll be able to compare offers from a half dozen or so different insurers. According to Kaiser data, however, this should be in line with what you’ll find.)

So, depending on the level of coverage one chooses (some levels have higher deductibles than others), it could be as little as $990 a year, which, in my example, is just a little less than 4% of household income. (This takes into account a $773 federal subsidy. Those who make less per year, obviously, would have larger subsidies.)

It’s been a while since I was 25 and shopped for insurance, but I’d be surprised to find that coverage could be had for 52% of $990, which is what Bentivolio stated above… Which brings me to an interesting question.

Is it legal for our elected officials to send politically motivated, completely unsubstantiated bullshit out to their constituents as facts?

Speaking of the “facts” as they concern Obamacare, I should add that Jeff Irwin will be participating in a town hall meeting about the rollout of Michigan’s health insurance exchange on Monday evening (September 30), along with the Director of U-M’s Center for Healthcare Research & Transformation (CHRT) Marianne Udow-Phillips, and the Executive Director of the Washtenaw Health Plan Ellen Rabinowitz. The meeting, which is to be held at the Mallett’s Creek Library (3090 East Eisenhower Parkway), will begin at 6:00.

Assuming some of you out there reading this are among the 50 million uninsured Americans (nearly 1.2 million of whom live in Michigan), I have a few more links and resources to share.

First, I’d suggest checking out the healthcare.gov tutorial on how to sign up for coverage come October 1.

Second, I’d suggest checking out the Washtenaw Health Plan. They’ve got good information online, but, more importantly, they’ve got an office at 555 Towner Street, in Ypsi, where they’ll be helping county residents to sign up in person. You just need to bring the required paperwork (which is outlined on their website), and show up Monday through Friday, from 9:00 AM to 4:00 PM, at their office.

Third, there are some good videos available online, which explain the ins and outs of the new system. The Keiser Foundation has one, as does the Washington Post. Here, for those of you who are interested, is the one from the Washington Post.

Fourth, the New York Times just posted an incredibly useful Q&A on these health insurance marketplaces. Here’s a taste…

Q: What are the penalties for not having coverage? Are there any exceptions?

A: Most people will be required to have insurance, with some exceptions. You are not required to buy insurance if: the cost of insurance premiums would exceed 8 percent of your income, your income is below the threshold for filing taxes, you have a certified hardship, or you would have qualified for Medicaid but live in a state that did not expand the program. Illegal immigrants, the incarcerated, members of Indian tribes and those who qualify for certain religious reasons are also exempt… Everyone else will pay a penalty. In 2014, it will cost you $95 or approximately 1 percent of your income, whichever is greater. The penalties will rise each year.

Fifth, check out the Keiser Foundaton calculator that I told you about above, so you can find out what kind of subsidy you might expect, how much you’d likely have to pay for coverage, and the likely size of your deductible.

Lastly, I just want to say how happy I am for all of you who, perhaps for the first time in your adult lives, will have insurance. This new system clearly isn’t perfect. You’ll still be expected to pay a great deal out-of-pocket when costly procedures and the like are called for, but those costs are capped, and, one would hope, this is just the first step on the path toward a much more efficient single-payer system. I know it’s confusing, even without all of the misinformation out there, but I’d encourage you to do some research and see what your options are.

And, to those who would say that this legislation wasn’t necessary, I’d remind you that more than 500,000 people in Michigan alone lost their private health insurance between 2008 and 2011, as more and more employers stopped offering coverage. The truth was, prior to Obamacare, insurance was becoming more difficult to come by, people were being dropped from their policies at the first sign of serious illness, and, as a result, our emergency rooms were being overrun, costing taxpayers a fortune. It was untenable. And everyone knew it. Unfortunately, politics got involved in what should have been a relatively simple matter. (Obamacare, contrary to what you might have heard, didn’t have its roots in socialist theory, but in a conservative think tank.) But conservatives decided to come out in force against it, as they did with every legislative initiative to come out of the White House under Obama, and it’s going to be their undoing. I’ve said it before, but they’ll rue the day when they decided to call this legislation “Obamacare,” instead of sharing credit for it. People are going to like it. Guess what? People like being able to get insurance when they have pre-existing conditions. They like being able to keep their kids on their insurance until they’re 26. And they like knowing that they can’t be dropped from their insurance when they’re diagnosed with cancer. These are good things. And they’ll forever be associated with Obama. Yes, it sucks to be told that you need to purchase insurance, but it also sucks to have to pay taxes, register for the draft, and do any number of things we’re expected to do as members of this society. Is this perfect? No. But it’s a hell of a lot better than what we had before.

And, with that, I’ll leave you with this quote from Obama… “The Republican party has just spun itself up around this issue… And the fact is the Republicans’ biggest fear at this point is not that Affordable Care Act will fail. What they’re worried about is it’s going to succeed.”

80 Comments

The Keiser link is very informative. So if I keep working, I’ll pay $25,000 a year to buy insurance on the exchange and pay out of pocket expenses – more than double my current cost. But if I quit working, I’ll only have to pay a maximum of $5000 a year for the same coverage. It will cost me $200,000 to continue working for another 10 years.

Are you getting insurance currently through your employer? If not, then I agree. You have a plan that is a good deal. If so, then half of the true cost of your insurance premium is being subsidized by your employer. Why half, and not a third or three quarters? Because half is where the employer derives the maximum tax advantage from offering you insurance in the first place. The only thing that seems high is the maximum out of pocket cost cap, but that makes the assumption that people making enough not to qualify for a federal subsidy (four times the poverty level) have enough money saved to cover such costs. Prudent financial planning would say yes, but actual data on savings rates would indicate no. Whether this is because of a lack of individual virtue or because of a structural economic weakness is unclear. Please discuss.

P.S. Bombing the crap out of everybody else a la WWII is not a realistic solution anymore. Comparative economic advantage is over. Get over it.

Four times the poverty level is about $62,000 per year. A family earning that amount pays the same amount for health care insurance under Obamacare as a millionare would. If anyone in the family smokes, there’s a 50% surcharge. This affordable health care would make a married couple who earn a combined $62,ooo a year pay $31,000 a year for insurance and out of pocket expenses if one of them smokes. 50% of their earnings for healthcare, another 20% for social security, and they are supposed to live and save for retirement using the 30% that is remaining. Or, they could just quit working and substantially improve their standard of living. How many people will continue to work at crummy jobs if the government confiscates 70% of their earnings?

Wonder if Obama is going to pay the smoking surcharge? Oh snap, I forgot. Our leaders in Washington have exempted themselves from Obamacare.

Why would the President, Congress or any other Federal employee need to buy insurance on the exchanges?

They receive insurance through their employer.

Ok, here’s an explanation:

http://politicalticker.blogs.cnn.com/2013/09/25/fact-check-congress-staff-are-exempt-from-obamacare/

The fact is that fewer Americans were insured and the associated costs were bankrupting society. Something had to be done. Prio to Obame, Republicans were saying the same thing. This was pure politics.

Republicans’ biggest fear is that it’s going to work and people will be happy.

It was easier to say its going to be better before they revealed the costs. Let’s look at a hypothetical 35 year old man who makes 40K a year, but is a contract laborer whose employer doesn’t pay for healthcare. Currently, $5000 a year for BCBS is too much. So, now under Obamacare he can get insurance for only $3,045 per year, but he will have to pay the first $6,350 out of pocket expenses before the insurance kicks in. So, the affordable care will be $4,400 more than what he considers too expensive today. Wonder how happy he will be?

Convenient that mark clipped his screen shot of his hypothetical example to exclude the out of pocket costs. Thats an extra $5200.

Gonna need a lot of fundraisers if someone ends up in the hospital.

“So, now under Obamacare he can get insurance for only $3,045 per year, but he will have to pay the first $6,350 out of pocket expenses before the insurance kicks in. ”

I don’t know where you’re getting your numbers from, but a 35 year old with a family would have to pay approx $206 per month under BCBS for the highest grade plan. He would have $10,000 in deductibles and be responsible for a max of $17,000 in out of pocket expenses.

That’s nearly twice what your situation under the ACA has. I can’t comment on the specifics of the plans.

How are these costs better than the current individual premiums offered by BCN?

http://www.mibcn.com/medicareAdvantage/individual-coverage/plans-and-benefits/plans-premiums-coverage-and-copayments.shtml

Would it be better to be status quo, where the subject pays nothing for health insurance, but has an unlimited amount of out of pocket costs in the event of a catastrophic illness? Maybe this is not perfect, but from an actuarial standpoint, only a few people in the aggregate insured pool will reach that limit in any given year, giving the remainder some time to adjust their financial planning so as to have some cushion of they should ever need it.

We should all urge success at this first attempt to unlink health insurance from employment. Employers are trying to pay less and less for health insurance, as the rate of increase of costs is rising much faster than net revenue. In the end, they want to be paying zero. Better to have a backup plan in place when this happens, rather than none at all. Only a very few people can bear 100% of all possible medical costs.

oops, my link is for the medicare plans.

Here is the link for a “young adult” (19-30) plan from BCBS.

http://www.bcbsm.com/index/2013-plans/michigan-health-insurance/affordable-health-insurance/young-adult-blue-max.html

$3500 max out of pocket (in network).

jcp2,

If we eliminated employer linked health insurance today, we could buy individual BCBS plans with a premium of $2616 and a maximum out of pocket of $3200. Why is it better to pay $25,000 through Obamacare?

I don’t know how the BCN plan you linked to compares, because you linked to a Medicare Advantage plan. Those costs do not include the costs of basic Medicare coverage, but are in addition to those costs. As the ACA is designed for people without access to health insurance (ie. under age 65), those that can enroll in a Medicare Advantage plan (65 and older) are automatically ineligible.

If your argument is that everybody should be eligible for BCN Medicare Advantage, and thus everybody should be eligible for Medicare, then I agree. We would have to work on scope of coverage, as Medicare as designed now is only for things that older people need. We would have to think of coverage for womens health, pediatrics, obstetrics, and so forth. Of course, this must mean you are really for single payer then, right?

My bad. I used Dan’s original link. But current costs for individual plans are significantly cheaper than Obamacare. Why is it better?

No, not single payer. Competition between insurance providers will insure costs remain low. BCBS can do it without denying coverage for pre-existing conditions. Other companies should be able to do likewise.

I agree that current costs are lower for individual plans through BCBS than projected through the ACA exchanges. However, BCBS of Michigan is currently loosing money through this service line. Despite this fact, BCBS has provided these plans as a provision of doing business in Michigan as a nonprofit entity, and as the largest third party insurer in the state. Recently, BCBS has converted into a for profit entity, and I do not anticipate these low rates to remain as low as they are now. In fact, over the next two or three years, I anticipate them to equilibrate with the rates from the Kaiser Foundation rate predictor site.

A retraction. BCBS has converted from a tax exempy non profit to a non profit mutual insurer, the same class as all the other third party insurers in the state. 2016 is the magic year when the current negotiated rate freeze between BCBS and the state expires. At that time, they will be free to change their rates to whatever the law allows at that time.

Is BCBS required by law to allow people with pre existing conditions?

As for competition, from here, it looks like the only company that EOS is familiar with is BCBS.

It is, in Michigan. I’m not that familiar with BCBS. I’m in a HMO. Very small out of pocket, but limited options where to obtain treatment.

If BCBS is all that’s available, there is no competition.

If you’re not that familiar with it, why are you commenting on it. You make yourself sound like an authority on every aspect of health care.

For a second, I was fooled.

I just did the Kaiser calculator and the calculator on the BCBS site.

The Kaiser calculator shows that a bronze plan is still cheaper than BCBS’s worst plan for the monthly premium ($100 vs. $168) and the out of pocket costs on the bronze plan are far cheaper ($4,500 vs. $27,000).

I don’t know, I might have this all wrong, but the bronze plan through the exchanges might be a better deal for me.

My mistake, these figures were for the Silver plan, not the Bronze plan.

Still, I think this might be a better deal. I’m not sure, though.

I wasn’t trying to hide the out-of-pocket expenses, Dan. I just couldn’t fit the entire thing in my screen capture. And, for what it’s worth, I actually think that a cap of $5,200 is a good deal, and one hell of a selling point. As I mentioned in a previous thread, my friend Patrick is facing a lot more than that right now, and his procedures weren’t terribly complicated. I don’t think it’s unusual at all for people to rack up bills upward of $100,000 these days, and I imagine that you could pass the $5,200 just a few minutes into a cancer surgery. So, no, I wasn’t trying to hide it.

EOS, if you don’t mind my asking, how much do you make a year that you’re projecting you’d have to spend $25,000 annually for insurance?

I just tried the Keiser calculator, plugging in information for a couple of 45 year old non-smokers with two kids, making a whooping $200,000 a year, and the annual expense was estimated at $10,362… Or less than half of what you say you’d owe. Do you really make on the order of half a million dollars a year?

Here’s what you said: “So if I keep working, I’ll pay $25,000 a year to buy insurance on the exchange and pay out of pocket expenses – more than double my current cost. But if I quit working, I’ll only have to pay a maximum of $5000 a year for the same coverage. It will cost me $200,000 to continue working for another 10 years.”

OK, EOS. I just plugged in information for a family of 6, making half a million dollars a year, and the calculator came up with an annual expense of $11,945… still less than half what you said the calculator told you that you’d owe. Were you reading it incorrectly, perhaps, or to you have several dozen children, and make millions a year?

To answer your questions, Numbers, it’s my understanding that, thanks to Obamacare, Blue Cross Blue Shield now has to accept people with preexisting conditions. That wasn’t the case previously, though. At least that’s what I’ve heard. (“Thanks, Obamacare!”)

And to those who say that Blue Cross Blue Shield has a better plan that’s cheaper, there’s nothing that says people have to use the ACA marketplace. If people want to buy insurance from BCBS, that’s awesome.

Also, can someone remind of the plan that the Republicans brought to the table? I mean, they voted to kill Obamacare 41 times, but what did they offer to take its place? I’ll answer that… They didn’t offer anything. They knew that the current system was untenable, but they offered nothing of their own. They were content to just sit by and watch the system crash. All they care about is power and political advantage. Again, I don’t thin Obamacare is perfect. I think we could have bargained, for instance to get prescription drug prices lower, but it’s a step in the right direction. It’s a big, cumbersome, ugly step, but at least it’s in the right direction.

Mark,

There is no subsidy for anyone making more than 4 times poverty. Someone making half a million dollars a year pays as much as someone making about $62,000 a year. Your still forgetting to include the out of pocket expenses. $12,050 a year for the premium and an additional $12,700 out of pocket. O.K. – I rounded up. Overestimated by $250 a year.

I believe EOS is including the total out of pocket expenses in to that figure of $25000.

What the Keiser calculator doesnt show is the actual deductible. According to an AP report, the average deductible for the silver plan would be about $2500. That means that the “insurance” company would not pay a dime of your medical expenses until you have paid $2500 yourself, and that is on top of the actual premium. The report mentions that the national average for premiums for the silver plan is expected to be $328/month. So youre looking at paying ~$6500 per year before you actually get insured for any medical expense. That would be the national average, anyhow. Obviously lower income people would pay less, however, the deductible is a lot higher in the “bronze” plan ($4500 on average)

http://news.yahoo.com/obamacare-trade-off-low-premium-high-deductible-210333482–finance.html

BCBS has been required to provide insurance to everyone regardless of pre-existing conditions for a number of years. It’s codified in Michigan law. Doesn’t have a damn thing to do with ObamaCare.

What did the Republicans do? They stood outside the locked Senate door while the Democrats came up with this train wreck. They weren’t allowed to read the Democrat plan before it was voted on. They were told that they had to vote for it before they found out what was in it. Reid refused to debate it, talk about it, or even explain how it would be implemented. They were told that no one who made less than $250K would have an increase in their taxes and the Supreme Court rued that this could be mandatory because it was a tax.

So what I’m taking home from this discussion is that, among all the possible variables of income, household composition, smoking status and zip code, we can cherry pick the one which shows that:

1) The Kaiser results are higher than BCBS

or

2) BCBS’s plans are highers than the ones on Kaiser

It all really depends on who is trying to say what.

Like Mark says, though, if you want to buy from BCBS, you can.

And just because Michigan required that BCBS take people with preexisting conditions (if s, great!), that doesn’t mean that the same law applies in Mississippi.

I’m also sensing that everyone posting here is just as uninformed as the next person (myself included). There’s nothing easy about health care, despite what one may like to believe.

All good reasons why the Democrats should slow down and delay the implementation of this law for at least a year. The Republicans are doing everything they can to make sure that this is discussed, debated, and fully examined before they force millions of people into health insurance programs that don’t fit their needs. If they fail, and Obamacare is implemented, then all the people who lose their jobs, or get their hours cut, or are required to change their personal physician, or wait months for necessary tests or treatments are sure to remember who is responsible during next November’s election. If its forced down our throats now, I predict a veto proof super majority in both the House and Senate, as the first year of its implementation will have significant challenges.

No, what they are afraid of, is that it’s going to work and they’ll be screwed in the mid-terms.

States have had years to prepare for this (you do realize that this bill was signed in 2010), and it’s been obstruction and foot dragging the whole way.

Contrary to being “forced down our throats,” the blame should really be thrown at lazy policy makers who were playing a fantasy that Romney would win in 2012 and America would turn into a nice Christian, right wing paradise.

Well, we can revisit this in a year and see which one of us is more delusional. I never thought Romney had a chance.

The plans are arranged as “Medal” levels (bronze, silver, gold, platinum) and that allows you to choose whether it is more important to you to have higher copays and deductibles (bronze) or lower copays and deductibles but higher monthly premiums (the others).

It’s important to note that if you are below 250% of the poverty level (in Mark’s example above) AND you pick a SILVER plan, you will be eligible for cost-sharing reductions on the copays and deductibles. (If you pick a bronze or gold plan, you won’t be…)

Also, if you are under 30 and generally healthy, there is a catastrophic plan available.

And you have some time to decide…

It’s not over yet. The Republicans could still shut down the government. It would be hugely unpopular, but they’ve done it before when they didn’t get their way.

The Atlantic has an interesting article on the ongoing battle over the debt ceiling and how ACA will be impacted.

I forgot the link.

http://www.theatlantic.com/politics/archive/2013/09/countdown-to-shutdown-a-primer-on-where-budget-wrangling-stands/280103/

Another article on The Atlantic. This one is about what happens now.

Read more:

http://www.theatlantic.com/business/archive/2013/09/not-raising-the-debt-ceiling-would-be-either-a-disaster-or-a-historical-calamity/280057/

“The American people don’t want a government shutdown, and they don’t want Obamacare,” House Republican leaders said in a statement over the weekend. “We will do our job and send this bill over, and then it’s up to the Senate to pass it and stop a government showdown.” Wrong. The only settled way we know what the American people want is through the democratic process. And the Affordable Care Act (Obamacare) is the law of the land. A majority of the House and Senate voted for it, the President signed it into law, its constitutionality has been upheld by the Supreme Court, and a majority of Americans reelected the President after an election battle in which the Affordable Care Act was a central issue. Moreover, we don’t repeal laws in this country by holding hostage the entire government of the United States.

The showdown over the budget and the debt ceiling is a prelude to 2016, when the Tea Partiers plan to run Texas Senator Ted Cruz for President. (Cruz, if you haven’t noticed, is busily establishing his creds as the biggest flamer in Washington – orchestrating not only the current extortion but also the purge of reasonable Republicans from the GOP.) We mustn’t give in to extortionists.

The Washington Post has a good Q & A too.

http://www.washingtonpost.com/blogs/wonkblog/wp/2013/09/30/%3Fp%3D63297/

Big news: Republicans just announced that they will only allow the federal government to stay open if President Obama agrees to delay implementation of Obamacare.

The New York Times says the announcement “all but assured that large parts of the government would be shuttered as of 12:01 a.m. on Tuesday.”

This is not a drill. After years of threats, Speaker John Boehner and the Tea Party are about to shut down the government for real, with millions of Americans losing access to vital services, hundreds of thousands of public servants unpaid, and a big blow to our economic recovery.

We can’t stop the Tea Party from trying to push America’s economy off a cliff, but we can make sure they pay a steep political price like they did in 1995 so that they finally stop this nonsense. Our plan is to start by putting targeted web ads on Facebook and other websites targeting the most vulnerable Republicans facing reelection next year and then keep up the pressure till the Republicans give up on these outrageous demands.

The Tea Party’s popularity has already sunk to near-record lows, and if the shutdown backfires, it could send the entire Republican Party into a tailspin. But time is of the essence—we need to raise $200,000 in the next 24 hours to power our rapid response campaigning and give us the ad budget we need to hold the Republicans accountable. Can you chip in $3 today?

The GOP has descended into chaos and infighting—literally yelling at each other on the Senate floor. The shutdown—while terrible for America—is a big opportunity to go on offense and send the Tea Party into permanent decline.

MoveOn has launched an ambitious campaign to discredit Tea Party Republicans and expose their 1% backers—to hold them accountable for threatening to sabotage our economy and trying to subvert our democracy. We’ll keep them on the defensive in the short term and ensure that no one forgets their reckless hijinks as elections approach next year.

After four straight years in which Tea Party Republicans have forced a job-killing austerity agenda down our throats, their reckless decision to risk a government shutdown finally has them on their heels. If they follow through, we’ll have a historic opportunity to expose just how extreme they are.

We’ll need to move quickly and speak forcefully to win the debate and bring about a repeat of 1995. That was the year Newt Gingrich and House Republicans shut down the government because they refused to negotiate with President Clinton. They paid for it dearly. Now, it’s on us to ensure this time is no different. If we play our cards right, 2013 could become known as the year the Tea Party relegated itself to the dustbin of history.

Our campaign includes rapid response ads and press outreach, as well as long-term strategies to discredit the Tea Party and take away its power, including pushing PBS stations to air “Citizen Koch,” the thus-far-censored documentary exposing the Koch Brothers as the Tea Party’s 1% financiers. We’ll also shine a spotlight on positive alternatives to the Tea Party’s agenda, including a higher minimum wage to tackle income inequality. And we’re amassing a war chest to ensure that this week is one everyone will remember well into next year. But first things first—the next few hours and days are crucial, and to win this fight, we all need to pitch in.

https://civ.moveon.org/donatec4/tea_partys_demise.html?rc=front

Together, MoveOn’s 8 million members have tremendous people power. Let’s go all in together to seize this opportunity and send the Tea Party packing.

Thanks for all you do.

–Anna, Carinne, Bobby, Alejandro, and the rest of the team

So as someone who is intimately familiar with the costs of self insuring in Michigan, our family of 3 currently pays $6,000/yr for one of the most affordable plans in MI I could find (not BCBS). In addition, we have a family deductible of $7,500 before the plan kicks in- so total potential out of pocket is $13,500. However, this plan does not cover prenatal/birth expenses, should I get pregnant again, nor prescriptions though it does offer an “Rx Club”. The “Rx Club”, until more recently when some of the provisions of Obamacare kicked-in, would not cover birth control (my largest medical expense at $1200/yr). According to the Kaiser calculator under Obamacare I would pay a premium of $5700 for the Silver level (70%) and out of pocket potential of 12,700 so a total of $18,400. So potentially I could be paying more out of pocket, but if I were to get knocked up, I would be covered under the Obamacare plan (to self-insure and have it cover pre-natal/birth the cheapest premiums are more than double what I currently pay). In addition, we are a pretty healthy family so we’ve never come close to meeting our deductible on our current plan. However, knowing that I have to pay $100 every time we have to go to the doctors office means we tend to avoid going. If I only had to pay $30, I would probably be more likely to go. Overall, for our family, if the numbers are correct, the Obamacare plan looks like it will be better a deal for our family.

I should also mention that trying to get my family self-insured after years of having employer coverage was one of the more frustrating, insulting, and embarrassing ordeals that I have had to endure. Hopefully this new system is less so.

I haven’t checked but I’ve heard that some things don’t require a deductible. Is that right?

Anne is, of course, a liberal plant.

However, if she hadn’t made so many bad choices in her life, she would have had a great plan from her employer.

XXX,

my understanding is that it depends on your state and county and plan. Some states give a waiver for the first few office visits before your deductible is applied. Some other services are exempt, but its all plan dependent.

I’m just shocked by the deductibles in these “Affordable” Care Act plans. Most people that didnt have insurance before can not afford upwards of $5000-$6000 PER YEAR in premiums and deductibles, before actually being insured.

If someone chooses the “Bronze” plan with an average of a $4500 deductible (on top of premiums), why in the hell would they get routine screenings and physicals? Basically any plan with a huge deductible is a “catastrophic” plan.

I suspect most people under 30 without employer subsidized health care will pay the $95 penalty. I suspect that most of those people would prefer to claim bankruptcy if needed, than pay that kind of money “just in case.”

Preventive health services for adults

Most health plans must cover a set of preventive services like shots and screening tests at no cost to you. This includes Marketplace private insurance plans.

Preventive care benefits

Preventive care helps you stay healthy. A doctor isn’t someone to see only when you’re sick. Doctors also provide services that help keep you healthy.

Free preventive services

All Marketplace plans and many other plans must cover the following list of preventive services without charging you a copayment or coinsurance. This is true even if you haven’t met your yearly deductible. This applies only when these services are delivered by a network provider.

Abdominal Aortic Aneurysm one-time screening for men of specified ages who have ever smoked

Alcohol Misuse screening and counseling

Aspirin use to prevent cardiovascular disease for men and women of certain ages

Blood Pressure screening for all adults

Cholesterol screening for adults of certain ages or at higher risk

Colorectal Cancer screening for adults over 50

Depression screening for adults

Diabetes (Type 2) screening for adults with high blood pressure

Diet counseling for adults at higher risk for chronic disease

HIV screening for everyone ages 15 to 65, and other ages at increased risk

Immunization vaccines for adults–doses, recommended ages, and recommended populations vary:

Hepatitis A

Hepatitis B

Herpes Zoster

Human Papillomavirus

Influenza (Flu Shot)

Measles, Mumps, Rubella

Meningococcal

Pneumococcal

Tetanus, Diphtheria, Pertussis

Varicella

Obesity screening and counseling for all adults

Sexually Transmitted Infection (STI) prevention counseling for adults at higher risk

Syphilis screening for all adults at higher risk

Tobacco Use screening for all adults and cessation interventions for tobacco users

Comprehensive coverage for women’s preventive care

All Marketplace health plans and many other plans must cover the following list of preventive services for women without charging you a copayment or coinsurance. This is true even if you haven’t met your yearly deductible.

This applies only when these services are delivered by an in-network provider.

Anemia screening on a routine basis for pregnant women

Breast Cancer Genetic Test Counseling (BRCA) for women at higher risk for breast cancer

Breast Cancer Mammography screenings every 1 to 2 years for women over 40

Breast Cancer Chemoprevention counseling for women at higher risk

Breastfeeding comprehensive support and counseling from trained providers, and access to breastfeeding supplies, for pregnant and nursing women

Cervical Cancer screening for sexually active women

Chlamydia Infection screening for younger women and other women at higher risk

Contraception: Food and Drug Administration-approved contraceptive methods, sterilization procedures, and patient education and counseling, as prescribed by a health care provider for women with reproductive capacity (not including abortifacient drugs). This does not apply to health plans sponsored by certain exempt “religious employers.”

Domestic and interpersonal violence screening and counseling for all women

Folic Acid supplements for women who may become pregnant

Gestational diabetes screening for women 24 to 28 weeks pregnant and those at high risk of developing gestational diabetes

Gonorrhea screening for all women at higher risk

Hepatitis B screening for pregnant women at their first prenatal visit

HIV screening and counseling for sexually active women

Human Papillomavirus (HPV) DNA Test every 3 years for women with normal cytology results who are 30 or older

Osteoporosis screening for women over age 60 depending on risk factors

Rh Incompatibility screening for all pregnant women and follow-up testing for women at higher risk

Sexually Transmitted Infections counseling for sexually active women

Syphilis screening for all pregnant women or other women at increased risk

Tobacco Use screening and interventions for all women, and expanded counseling for pregnant tobacco users

Urinary tract or other infection screening for pregnant women

Well-woman visits to get recommended services for women under 65

I’m disappointed. I had thought that Dan and EOS knew everything there was to know about Obamacare.

Oh wait, there’s even more:

Coverage for children’s preventive health services

All Marketplace health plans and many other plans must cover the following list of preventive services for children without charging you a copayment or coinsurance. This is true even if you haven’t met your yearly deductible.

Autism screening for children at 18 and 24 months

Behavioral assessments for children at the following ages: 0 to 11 months, 1 to 4 years, 5 to 10 years, 11 to 14 years, 15 to 17 years.

Blood Pressure screening for children at the following ages: 0 to 11 months, 1 to 4 years , 5 to 10 years, 11 to 14 years, 15 to 17 years.

Cervical Dysplasia screening for sexually active females

Depression screening for adolescents

Developmental screening for children under age 3

Dyslipidemia screening for children at higher risk of lipid disorders at the following ages: 1 to 4 years, 5 to 10 years, 11 to 14 years, 15 to 17 years.

Fluoride Chemoprevention supplements for children without fluoride in their water source

Gonorrhea preventive medication for the eyes of all newborns

Hearing screening for all newborns

Height, Weight and Body Mass Index measurements for children at the following ages: 0 to 11 months, 1 to 4 years, 5 to 10 years, 11 to 14 years, 15 to 17 years.

Hematocrit or Hemoglobin screening for children

Hemoglobinopathies or sickle cell screening for newborns

HIV screening for adolescents at higher risk

**Hypothyroidism screening for newborns

Immunization vaccines for children from birth to age 18 —doses, recommended ages, and recommended populations vary:

Diphtheria, Tetanus, Pertussis

Haemophilus influenzae type b

Hepatitis A

Hepatitis B

Human Papillomavirus

Inactivated Poliovirus

Influenza (Flu Shot)

Measles, Mumps, Rubella

Meningococcal

Pneumococcal

Rotavirus

Varicella

Iron supplements for children ages 6 to 12 months at risk for anemia

Lead screening for children at risk of exposure

Medical History for all children throughout development at the following ages: 0 to 11 months, 1 to 4 years , 5 to 10 years , 11 to 14 years , 15 to 17 years.

Obesity screening and counseling

Oral Health risk assessment for young children Ages: 0 to 11 months, 1 to 4 years, 5 to 10 years.

Phenylketonuria (PKU) screening for this genetic disorder in newborns

Sexually Transmitted Infection (STI) prevention counseling and screening for adolescents at higher risk

Tuberculin testing for children at higher risk of tuberculosis at the following ages: 0 to 11 months, 1 to 4 years, 5 to 10 years, 11 to 14 years, 15 to 17 years.

Vision screening for all children.

$6400 for my family and I in new costs that will not go toward my children’s college education fund.

Where did you get your insurance before?

Why does that matter? What matters is what I said – I will be spending my money on something I don’t want that I feel would be better served elsewhere.

It matters if your insurance was free before.

So, are you saying that you don’t want health insurance? Then don’t buy it.

I think I may wind up taking the penalty – if this goes as planned, it’ll be there when I need it.

Your family’s health is obviously your business, but that would be pretty silly.

Paying the penalty doesn’t insure that all of your health care costs are automatically covered. As it says below, you are responsible for all of your costs of care.

I’m assuming that you don’t have insurance now, though, anyway. Obviously, you are used to taking the risk.

This is from the healthcare.gov site:

“What if someone doesn’t have health coverage in 2014?

Email

PRINT

If someone who can afford health insurance doesn’t have coverage in 2014, they may have to pay a fee. They also have to pay for all of their health care.

When the uninsured need care

When someone without health coverage gets urgent—often expensive—medical care but doesn’t pay the bill, everyone else ends up paying the price.

That’s why the health care law requires all people who can afford it to take responsibility for their own health insurance by getting coverage or paying a penalty.

People without health coverage will also have to pay the entire cost of all their medical care. They won’t be protected from the kind of very high medical bills that can sometimes lead to bankruptcy.

The fee in 2014 and beyond

The fee in 2014 is 1% of your yearly income or $95 per person for the year, whichever is higher. The fee increases every year. In 2016 it is 2.5% of income or $695 per person, whichever is higher.”

It’s also important to note, that the preventative services listed above would not be free, either.

I don’t know, if it were me and I had kids, I’d buy an insurance plan.

You seem like you are pretty used to living with the risks, though.

Now, I am admittedly underinformed about the flora and fauna of the bill, but as I read this, I wonder – at my stage in life, is it truly worth it? I’m screwed if I, say get into a massive car accident and they decide to keep my brain wired alive (even though I have a living will preventing this), but if I come down with a terminal illness, can’t I just buy into it then, based on the premise that no one can be turned down, which I was made to believe was a major point of this law?

You could, but it probably would not pay for your bills retroactively.

Obviously, insurance is inherently a gamble, but for a car wreck, most of your expenses would probably be incurred before you have a chance to apply for insurance.

As for a condition like a major heart attack, you could be put in the same boat.

The penalty is obviously intended to make up for people who might wait until something happens to get insurance.

In a catastrophic event, the worst case for you, would be not to die, but even dying wouldn’t get your family off the hook. You might have a life insurance policy to take care of that though.

I don’t know, at this stage of my life, I kind of know better. Even if you are young and healthy, it’s not hard to run up thousands of dollars worth of medical expenses in a year.

I’m not sure where the $6400 is coming from. That would be a total of the premium and deductibles.

If you aren’t using medical care anyway, it would make sense to have at least some kind of policy. You would only have to pay the premiums, which wouldn’t be all that much more than the penalty. Plus you could get the free services for you and your family.

I’m just assuming that since you don’t have insurance right now, that you don’t make a whole lot of money and would pay a small premium. On my small salary, I would only have to pay about $1500 a year.

If you make enough to pay a $6400 premium, then there’s no reason you shouldn’t have insurance.

This debate really does reflect how fucked up health care is in this country. Insurance companies, big pharma, and doctors continue to make money hand over fist while we can’t find a reasonable way to provide basic healthcare for our citizens like every other civilized nation can. This is a fucked up law that is a band-aid that doesn’t cover the wound. I, for one, think that single payer is the way to go ultimately. Without that being an option right now, I happen to agree with an earlier statement that EOS made … Well, we can revisit this in a year and see which one of us is more delusional…

Lets see if this is a good law or not. If not, the world won’t end nor will the healthcare system collapse. If it is as bad as many on the right believe, time will tell.

This is small potatoes compared to the debt ceiling debate. That will have devastating effects.

Numbers,

I never claimed to be an authority on this bill, any more than Mark did when he posted his hypothetical numbers. I merely posted hypotheticals as well.

I’m extremely glad that a good number of preventative measures are covered (prior to deductible), otherwise, I would see no point in paying that kind of money essentially for a catastrophic policy. But these numbers and this info hall all just literally been released. There is an extraordinary amount of information that the public hasnt even had the chance to digest.

But my point was basically that this “affordable” care act isnt really any more affordable than what was previously available.

IMO, THE huge improvement is on the mandate to allow pre-existing conditions. Thats an extreme step forward for the country, even though some states like ours already required that. The cap on year-to-year increases is also a great thing, as is the inherent competition.

I just dont get what people are acting like “for the first time, I can buy insurance.” Unless the previous condition thing was keeping you from buying it, you didnt buy it because it was too expensive. And it’s still too expensive, likely even more so.

The more I look in to what’s on the exchanges, the better it looks to me.

Single payer systems aren’t the only way to go. Germany and Japan are two countries which rely heavily on the private sector to provide both health insurance and health care. Both of those countries, however, strictly regulate their health care sectors to control prices and provide minimal state care to extremely poor people. Neither of those countries, however, has near the level of inequality we do.

I can’t ever seen the States moving to a single payer system (though we do have them: Medicare, we even have socialized medicine, the VA and the Indian Health Service). Certainly, it makes a whole lot of sense to do so, but it would be a nightmare to try to get it through Congress.

I’m finding these prices on the Kaiser website completely reasonable, particularly for low income and low middle income households, who often have to do without insurance anyway. Either that or they have substandard plans which don’t provide all the free services listed.

As a contract worker, I’m relieved that there are options available finally. Certainly BCBS would take anyone, but every time I tried to sign up in the past, the prices always ended up being much more than I could afford. Fortunately, I was lucky enough to have not had a car accident or become majorly ill. I would never live like that again, however. It’s entirely stupid to not have some type of health insurance, assuming one can afford it.

Peter,

” It’s entirely stupid to not have some type of health insurance, assuming one can afford it.”

this we agree on 100%. There are practically no people that have a mortgage and do not have insurance on their home. But there are millions that do not have insurance on their bodies.

I know it’s required to have homeowners insurance, and thats a big reason why I supported this bill (before I saw the deductibles). Forcing everyone to be insured protects our economy. I’m not sure how I feel about this bill right now, after seeing the numbers, but there are some good things in it. I just think with $4500-ish deductibles + premiums in the plans aimed at the poor, i think many may opt for the penalty.

Certainly, I also wish there were no deductibles, but we can’t always get what we want.

As Numbers pointed out, the penalty doesn’t cover medical costs. You still end up having to pay them, the insurance you enter following the event won’t cover expenses retroactively and you can’t take advantage of preventative services.

It’s not perfect, but it’s better than what we had before. Even with the deductibles, for those who don’t use medical care, they’ll never know they are there. For those that end up having to, they can at least avoid bankruptcy (which is no cakewalk at all).

The very poor have access to Medicaid, the not so poor (under 30K) can insure their family for $600. Even with a $4500 (or more) deductible, that’s entirely reasonable.

Like I said above, heath care in Germany and Japan is privately provided and it most certainly isn’t free. It’s definitely cheaper than here, though. I’m not sure what kind of plan everyone is hoping for. I can’t see a Canadian system working here.

I know it’s easy to say that insurance could have been bought before, but, like I said, I tried many times and couldn’t find anything for less than $800 a month for the family, and that still included deductibles. I also worked for small businesses who desperately tried to get policies for their employees, but it never worked out. It was just simply too expensive.

Just received an email from the White House about the government shutdown that’s looming and I thought that the following sentence might be of interest.

“In fact, shutting down the government won’t stop Obamacare. The Health Insurance Marketplace will still open for business starting tomorrow, without delay.”

Mark,

have these crooks told you if they have a snow day tomorrow or now?

A little good news today — I hear the exchanges have been swamped.

New Republic Senior Editor John Cohn was on Reddit answering questions about Obamacare.

Read more:

http://www.reddit.com/r/IAmA/comments/1niguh/im_jon_cohn_a_senior_editor_at_the_new_republic/

New York Times breaking news alert.

Read more:

http://www.nytimes.com/news/fiscal-crisis/2013/10/01/from-rose-garden-obama-blames-shutdown-on-house-republicans/?emc=edit_na_20131001

Part of the problem with the site’s launch stemmed from the fact that it was being hit by conservative Denial of Service attacks.

Read more:

http://www.examiner.com/article/right-wing-cyber-attacks-on-healthcare-gov-website-confirmed

Suck it, EOS.

Read more:

http://www.nytimes.com/2014/04/18/us/obama-says-young-adults-push-health-care-enrollment-above-targets.html?emc=edit_na_20140417

Remember when they sold us this they claimed 40 million uninsured would be covered? The problems signing up will be nothing compared to the problems implementing the healthcare. The only good result is that Democrats will be out of power for the foreseeable future.

It sure does suck.

http://washingtonexaminer.com/poll-most-americans-believe-obama-lies-on-important-issues/article/2547367